Quarterly Investment Update – 1st Quarter 2025 – Financial Services

PC

Perkins Coie LLP

Perkins Coie is a premier international law firm with over a century of experience, dedicated to addressing the legal and business challenges of tomorrow. Renowned for its deep industry knowledge and client-centric approach, the firm has consistently partnered with trailblazing organizations, from aviation pioneers to artificial intelligence innovators. With 21 offices across the United States, Asia, and Europe, and a global network of partner firms, Perkins Coie provides seamless support to clients wherever they operate.

The firm’s vision is to be the trusted advisor to the world’s most innovative companies, delivering strategic, high-value solutions critical to their success. Guided by a one-firm culture, Perkins Coie emphasizes excellence, collaboration, inclusion, innovation, and creativity. The firm is committed to building diverse teams, promoting equal access to justice, and upholding the rule of law, reflecting its core values and enduring dedication to clients, communities, and colleagues.

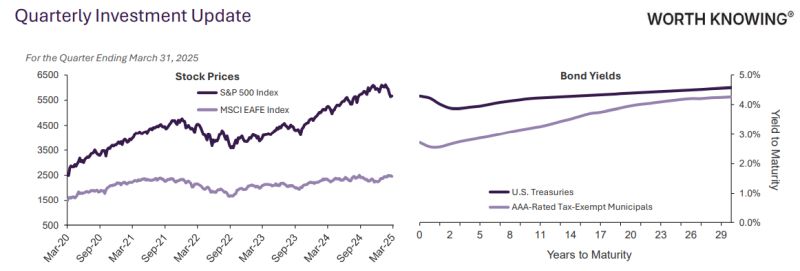

The rally in U.S. stocks came to an abrupt halt as uncertainty around tariffs, fiscal policy, and future economic growth put investors on edge.

United States

Finance and Banking

To print this article, all you need is to be registered or login on Mondaq.com.

Stock Market Commentary

The rally in U.S. stocks came to an abrupt halt as uncertainty

around tariffs, fiscal policy, and future economic growth put

investors on edge. Technology and consumer discretionary stocks,

two of the best-performing sectors last year, were particularly

hard hit. The tech-heavy Nasdaq Composite Index and the broader

S&P 500 Index both fell into correction territory, declining

over 10% from their peak and ultimately ending the quarter down 10%

and 4.3%, respectively.

Despite the dour headlines, not all markets were negative.

International stocks, aided by a weakening U.S. dollar, posted

robust gains. The MSCI EAFE Index, which tracks the performance of

companies in developed markets including Japan and Europe, ended up

7%, the largest quarterly outperformance versus U.S. stocks since

2002. The MSCI Emerging Markets Index, which includes countries

such as China and India, also rose, up 3%. Even in the United

States, 7 out of 11 sectors were positive, led by energy and

healthcare.

While economic uncertainty and market volatility may remain

elevated in the near term, we continue to emphasize the importance

of diversification and periodic rebalancing. U.S. stocks,

particularly large technology companies, have been market leaders

in recent years, but investable opportunities do exist outside that

segment of the market.

Bond Market Commentary

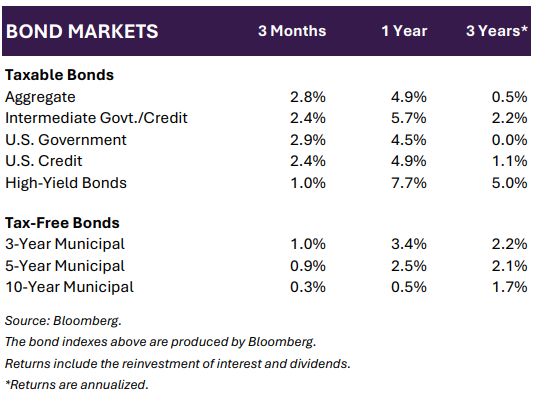

In the first quarter of 2025, the fixed income market performed

well as a risk diversifier, with the Bloomberg US Aggregate Bond

Index rising 2.8% year-to-date. However, like equities, bond

markets experienced notable volatility due to the threat of

significant tariffs. These tariffs raised investor concerns about

higher inflation and slower economic growth, prompting a shift to

favor short-duration assets and a more defensive tactic in the

fixed income market.

As a result, corporate bond spreads widened in the first three

months of 2025. Highyield bond spreads spiked 78 basis points (bps)

from their January low, before tightening slightly, while

investment-grade spreads followed a similar pattern, rising

modestly by 15 bps since February.

The U.S. Federal Reserve acknowledged the rising risks to

economic stability and responded by maintaining the federal funds

rate at 4.25% to 4.5% and adopting a cautious approach. Other

central banks, however, adopted more aggressive policies for 2025.

Citing uncertainty over the impact of U.S. trade policies, the

European Central Bank, Swiss National Bank, and Bank of Canada each

cut their target rates by 25 bps in March.

Economic Commentary

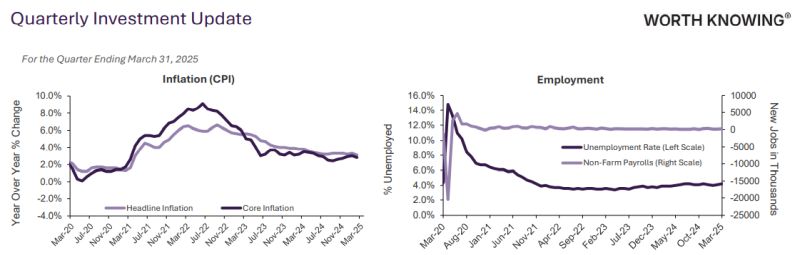

In the first quarter of 2025, the U.S. economy found itself at a

crossroads, balancing modest growth against the rising pressures of

inflation and shifting global trade dynamics as various tariffs

went into effect, with the president estimating $600 billion in

tariff revenue per year, or 1.8% of current gross domestic product.

Inflation remained a pressing concern as the core Personal

Consumption Expenditures (PCE) price index, a key inflation

indicator, rose 2.8% year-over-year, slightly above

expectations.

In January and March, the Federal Reserve opted to hold interest

rates steady, saying it is in no hurry to lower them in the current

climate of uncertainty. The U.S. unemployment rate also held fast

at 4.2%, combating expectations of higher unemployment in light of

government job cuts linked to policy changes from the Department of

Government Efficiency.

Consumer sentiment dropped notably, with the University of

Michigan’s consumer sentiment index reporting a 12% plummet

from February to March across all demographics, marking its third

consecutive month of decline. Expectations of less-stable personal

finances, tariffs and their potential economic impact, higher

unemployment, and persistent inflation all contributed to the

decrease. Although uncertainty played a role in the erosion of

consumer sentiment and other soft data, the hard data show a more

stable picture as we head into the second quarter.

The content of this article is intended to provide a general

guide to the subject matter. Specialist advice should be sought

about your specific circumstances.

link