Here’s Why Crocs (CROX) Stock is a Lucrative Investment Bet

Stock is a Lucrative Investment Bet")

Crocs, Inc. CROX seems promising, thanks to robust business strategies. The company has been gaining from solid consumer demand across the Crocs and HEYDUDE brands, backed by effective pricing actions. It has also been seeing strength in clogs, sandals and personalization. In first-quarter 2024, its bottom line surpassed the Zacks Consensus Estimate for the 16th consecutive time.

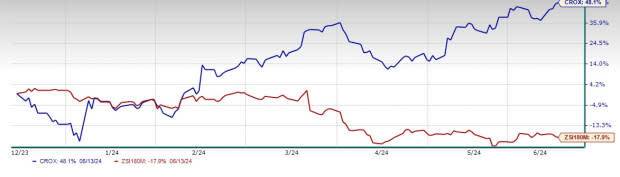

Buoyed by such upsides, this currently Zacks Rank #2 (Buy) company has gained 48.1% in the past three months against the industry’s 17.5% decline.

Let’s Delve Deep

Crocs has been witnessing a decline in inbound freight costs, which has been contributing to gross margins for quite some time now. Also, favorable product costs, along with select price increases internationally and lower discounting have been acting as tailwinds. In the first quarter, the adjusted gross profit rose 9.6% year over year while the adjusted gross margin expanded 180 basis points to 56%, owing to gains from lower freight costs across both brands.

The company’s classic clogs are serving as a significant driver, attracting both new customers and retaining existing ones. Additionally, the double-digit growth in the kids’ business was another highlight for the quarter. Management continues to view personalization as a mega consumer trend, with the opportunity of expanding the Jibbitz penetration in 2024 via higher penetration within digital and wholesale channels, consistent product freshness innovations and advanced speed to market capabilities.

Image Source: Zacks Investment Research

Crocs is on track with its long-term strategy and key initiatives to deliver sustainable growth. Its growth strategy is focused on three key initiatives. The first key initiative is igniting icons to enhance brand awareness and relevance. The second is investing strategically in Tier 1 markets to drive market share gains via talent, marketing, digital and retail. The third initiative is diversifying the product range to attract new consumers.

Backed by the strong first-quarter performance and expectations of continued strength across its brands, Crocs outlined a robust view for second-quarter and full-year 2024. Additionally, the company is confident of its strategies and investments, which are expected to drive market share gains. For the second quarter, Crocs expects revenues to be up in the band of 1-3% from the year-ago levels at constant currency. Revenues are likely to grow in the range of 7-9% from the prior-year actuals for the Crocs brand and plunge 17-19% for the HEYDUDE brand. The company expects adjusted earnings to be in the range of $3.40-$3.55 per share and the adjusted operating margin to be 26.5%.

For 2024, Crocs anticipates revenue growth in the range of 3-5% from the year-earlier levels at constant currency. Revenues are expected to rise in the band of 7-9% for the Crocs brand and decline 8-10% for the HEYDUDE brand. However, the company expects HEYDUDE sales trends to improve each quarter, with the normalization of the sell-in and sell-through dynamic into the fourth quarter. It anticipates gross margin to improve from a year ago at the enterprise level, with gross margin growth across the Crocs and HEYDUDE brands. The company anticipates an adjusted operating margin of 25%, with adjusted earnings per share in the range of $12.25-$12.73.

To wrap up, Crocs seems to be an attractive investment bet given all the aforementioned positives.

Other Solid Picks

Some other top-ranked companies are G-III Apparel Group GIII, Royal Caribbean RCL and lululemon athletica LULU.

G-III Apparel Group sports a Zacks Rank #1 (Strong Buy), at present. You can see the complete list of today’s Zacks #1 Rank stocks here.

G-III Apparel Group has a trailing four-quarter earnings surprise of 571.8%, on average. The Zacks Consensus Estimate for GIII’s fiscal 2024 sales indicates an increase of 3.3% from the year-ago period’s reported level.

Royal Caribbean sports a Zacks Rank of 1, at present. RCL has a trailing four-quarter earnings surprise of 18.3%, on average.

The consensus estimate for RCL’s 2024 sales and earnings per share (EPS) indicates increases of 16.8% and 63.8%, respectively, from the year-ago period’s reported levels.

lululemon athletica is a yoga-inspired athletic apparel company. LULU carries a Zacks Rank # 2, at present.

The Zacks Consensus Estimate for lululemon athletica’s current financial-year sales and EPS indicates growth of 11.4% and 11.8%, respectively, from the year-ago corresponding figures. LULU has a trailing four-quarter earnings surprise of 7.4%, on average.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Royal Caribbean Cruises Ltd. (RCL) : Free Stock Analysis Report

lululemon athletica inc. (LULU) : Free Stock Analysis Report

Crocs, Inc. (CROX) : Free Stock Analysis Report

G-III Apparel Group, LTD. (GIII) : Free Stock Analysis Report

To read this article on Zacks.com click here.

Zacks Investment Research

link