ECD Automotive Design: Hello Small-Cap World (NASDAQ:ECDA)

")

Sjo

Today, I write to share an under-the-radar and very compelling micro-cap equity, ECD Automotive Design, Inc. (NASDAQ:ECDA). Chances are you never heard of the stock. And unless you are a mover and a shaker, with lots of disposable income (and/or serious wealth), you might not yet be familiar with the company’s products. Therefore, given my relatively large small-cap following, this is ECDA’s introduction to the broader micro-cap investing world.

Small Cap & Micro-cap world, please meet ECDA.

To get right to it, here is why I find ECDA shares so compelling.

ECD Automotive Design, Inc. is a custom builder of classic and restoration motor vehicles. The company spends roughly 2,200 hours, per custom-built vehicle, to build 1-of-1 restorations with all the modern features desired by its clients. For example, its Land Rover Defenders can have an electric engine, a Corvette engine, or a different engine. From one-of-a-kind paint colors to unique leathers to a multitude of features and accessories, the world is the client’s oyster here. Generally, this is a seven to nine-month process, depending on how quickly the client moves along the various selection and design phases. Throughout the journey, the client receives white glove treatment and feels part of the process because they get to design a truly unique and custom version, again, a 1-of-1 vehicle, perfectly suited to their exacting tastes.

ECDA is among the largest restoration companies of Land Rovers and offers a Jaguar E-Type line. Recently, they have secured the licensing rights to build the Toyota Motor Corporation (TM) FJ 40/ 60 Cruiser, as well as the rights to make custom restorations of the 1967 and 1968 Ford Motor Company (F) Mustangs. Production of its first FJ Cruisers and Mustangs is scheduled for Q4 FY 2024 and early 2025. Given the much larger addressable market for both the FJ Cruiser and Mustang, this should be a big driver of FY 2025 revenue growth. In addition, this makes sound business sense, as it enhances the diversity of ECDA’s product mix, and casts a wider net, ultimately, playing in much larger addressable markets.

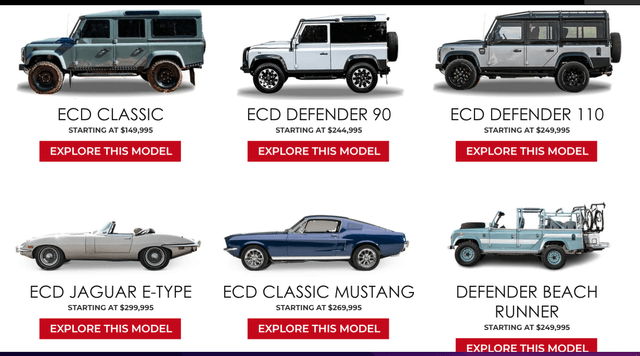

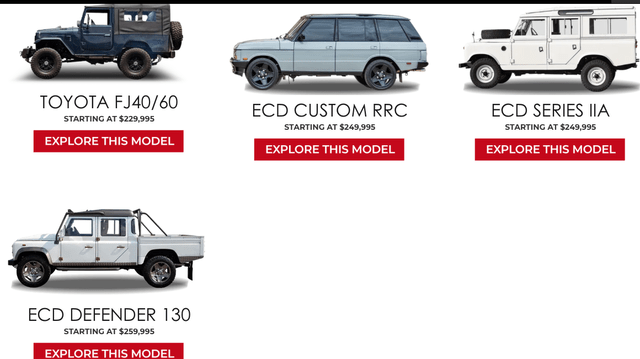

Enclosed below are the current model types available for customer purchase.

E.C.D. Automotive Design, Inc. E.C.D. Automotive Design, Inc.

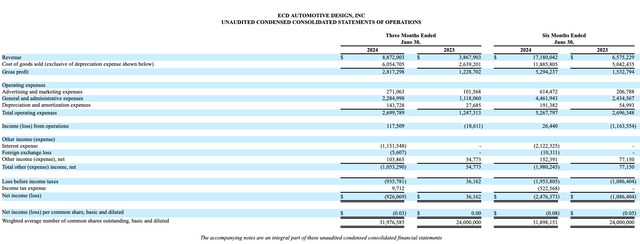

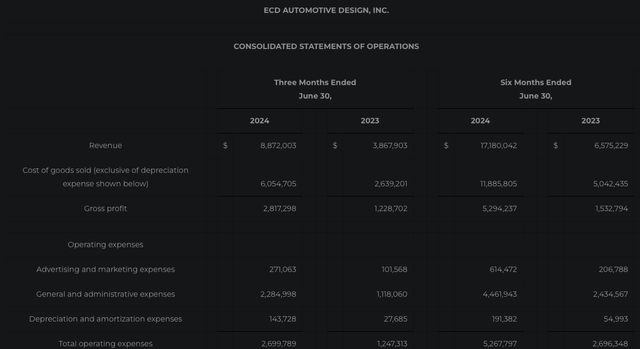

In terms of the business and what the financials look like, the company is growing its revenue rapidly, at a 100% plus pace, in FY 2024. It has among the best gross margins in the automotive industry, only trailing its publicly traded peer, Ferrari N.V. (RACE).

Last night, the company reported 129% YoY Q2 FY 2024 revenue growth and positive Adj. EBITDA. On the company’s conference call, management suggested that it has the potential to grow to upwards of $65 million in revenue. Its state-of-the-art Kissimmee, FL factory, if /when they can drive demand to capacity, could handle 180 vehicles per year.

For perspective, ECDA’s FY 2024 guidance is 98 vehicles. So, given the economies of scale, growing from 98 to 125 or 150 vehicles should be more profitable, driven by operating leverage and higher capacity utilization rates. Furthermore, when asked during last night’s analyst Q&A portion of the conference call, management indicated its backlog is very robust.

Risks

As this is a micro-cap security, with only about a $38 million market capitalization, of August 19, 2024, the risks section is lengthier than usual.

Despite growing its revenue at 129%, in Q2 FY 2024, compared to the year ago period, exhibiting a very healthy gross margin, and posting positive income from operations, quarterly interest expense of $1.15 million drove ECDA to a Q2 FY 2024 quarterly net loss, of $926K. On this cash burn trajectory, the company has a cash runway of about 7 quarters of cash burn, depending on your assumptions, post its August 2024 small $2 million capital (which will be discussed in greater detail, later in the piece).

ECDA Q2 FY 2024 10-Q

Secondly, on Friday, August 16, 2024, the company disclosed that its Nasdaq Global Market listing was in jeopardy. However, per its CFO, as I confirmed with the company this morning, ECDA could move from the Nasdaq Global Market to the Nasdaq Capital Market once ECDA’s stock closes at a price higher than $1.01 for 10 consecutive days.

In addition to the two larger risks, highlighted above, enclosed please find a few other risks to consider.

- ECDA is a micro-cap stock that often has limited average daily trading volume.

- ECDA is selling a luxury product to a very wealthy clientele, so although they may be relatively immune to economic downturns, given their clients’ wealth, any major and negative changes to the macro outlook could slow growth.

- The company has to prove it can successfully ramp up and produce the FJ Cruiser and Ford Mustangs, at the same level as the craftsman of its Land Rover and Jaguar lines.

- The company has to manage its working capital dollars well to scale its second half FY 2024 and FY 2025 revenue growth.

The Peter Lynch Inspired/Style Research

Incidentally, taking a page out of Peter Lynch’s playbook, this past July 2024, I had a good excuse to take with my wife a short weekend getaway vacation and attend the 3rd annual Defender rally. This was held on beautiful Nantucket, right outside the Cisco brewery. During our visit to the island, I got to test drive one of ECDA’s Defenders, thus literally kicking the tires, in person, as well as spending time meeting and speaking with some members of ECDA’s management team, notably its CEO. I was impressed on all fronts.

Enclosed below are a few pictures from my visit:

ECD Defender Beach Runner:

Author’s photo

ECD Classic:

Author’s photo

The back:

Author’s photo

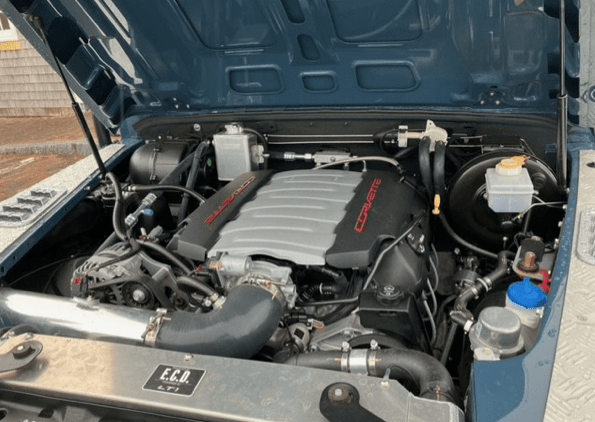

The Engine:

Author’s photo

There are a few other additional photos in the archives section.

Brief History:

The company was founded in 2013 by Scott Wallace and members of the Humble Family. Scott, who I’ve met with and spent two hours speaking with, while on Nantucket, is intelligent, hard-charging, and has an impressive and proven track record of private equity investing successes, in Europe. He walked me through his two best and most lucrative deals and the clever thought process for acquiring the assets, how they greatly enhanced and grew the businesses, and how they then sold the businesses, for a very handsome return. This was done over an approximately three to four-year time span, per investment. The Humble family are gear heads and passionate about the product/ craftsmanship and fostering the right employee culture.

During our conversation, what jumped out was ECDA’s strong mechanic retention rates, nearing 100%, which is very impressive compared to the usual high turnover rates experienced by many other segments of the automotive mechanic world. ECDA does a good job of attracting and retaining its collection of highly skilled mechanics by paying them well. They receive ownership and autonomy, allowing them to play an integral part in the build, thus doing what they love best, practicing their craft and art form.

The company went public, in December 2023, via a SPAC. However, the deal was deeply undersubscribed, due to the initial/ implied valuation, such that the vast majority of pre-SPAC holders elected to redeem their shares back, at $10, via the SPAC put option.

Valuation

As of August 17, 2024, and post a minimal PIPE, raising $1 million of equity, at $1 per share, in August 2024, ECDA has 34.65 million shares outstanding. As of June 30, 2023, the company had $5.6 million in cash. On a pro forma basis, as of August 19, 2024, the company raised $2 million, $1 million in equity (referenced above) as well as $1 million of incremental debt. This additional capital is earmarked for incremental working capital to build a modest number of spot vehicles (for customers that don’t want to wait seven to nine months and want to buy a vehicle sooner rather than later) as well as ramp up production of its upcoming Toyota FJ Cruiser and Ford Mustang lines.

At yesterday’s closing price, of $1.10, we are talking about a market capitalization of only $38.2 million. ECDA has a $16.8 million Convertible Preferred Note outstanding, which is accruing interest at SOFR +600 bps and the strike price or conversion price is $2 per share. On a pro forma basis, we are talking about roughly $10 million of net debt.

During Q2 FY 2024, the big ramp in revenue growth led to a lot more gross margin dollars. However, because the company is still growing rapidly as well as shouldering additional expenses, associated with being a recently newly publicly traded company, there should be further signs of positive bottom line operating leverage. That is, if and when they can ramp up FY 2025 production and units.

ECDA’s Q2 FY 2024 Earnings Press Release

The Float

Upon the registration of the recently issued 1 million shares, sold to a strategic and long-term investor, the entire public float of ECDA is only 6 million shares. North of 28 million shares are controlled by insiders and the SPAC sponsor. Please note that until ECDA’s S-3 is officially registered, the 180-day lock-up clock doesn’t start to tick, again for any of the insiders, as their shares aren’t registered. It is my understanding that ECDA’s convertible preferred holder, ATW Partners, also owns roughly 2 million shares of equity, not including roughly 8.4 million shares that could be converted, at $2 per share, if ATW were to exercise the conversion option.

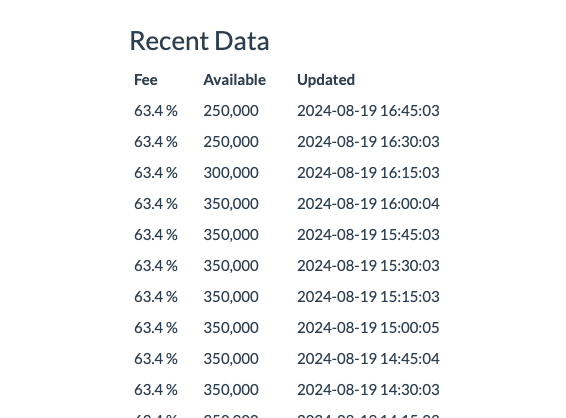

According to Iborrowdesk.com, as of August 19, 2024, the cost to borrow shares of ECDA, to short the stock, was 63.4% annualized.

Iborrowdesk.com

Incidentally, last night, in after-hours, post the 4 PM release of ECDA’s earnings, ECDA shares quickly shot up, with a high watermark, reaching $1.70 per share. Then quite strangely, every bid got hit, and a lot of volume traded between $1.60, all the way down to $1.15, then suddenly, trading volumes slowed dramatically. Candidly, I’m scratching my head here, as ECDA’s public float is only 5 million total shares (as I don’t believe the new 1 million share PIPE shares have yet been registered, and the PIPE buyer is a long-term holder) and I believe ATW Partners owns rough 2 million out of the five million shares. I can’t work out where that amount of stock was actually located, and so quickly, with most of the action taking place between 4:01 PM and 4:20 PM. Again, how can nearly 1 million shares trade when the entire public float is only five million shares?

My only plausible explanation is a combination of profit taking, by short-term traders, and short selling, hence the 63.4% borrow rate, as of last night.

Nasdaq.com

That said, who the heck is crazy enough to short a company with a tiny float, of only 6 million shares (upon the registration of the small $1 million PIPE)? After all, this is a company that is growing its revenue north of 100%, just posted positive Adj. EBITDA, and has a strong pipeline and backlog of growth, for the second half of 2024 and well into 2025 with the FJ Cruiser and Ford Mustang lines.

If the company can successfully ramp up its unit volume, at comparable gross margins, this should drive more absolute gross margin dollars. As the business scales, the Opex should grow much more slowly, thus driving more operating income to cover the debt and march towards the Rubicon of EPS profitability.

Putting It All Together

It is very difficult to find micro-caps equities that are growing revenue north of 100%, have industry-leading gross margins, qualitatively make great luxury products, and that just inflected to positive Adj. EBITDA. I would argue that ECDA, the stock and the product, are relatively unknown, and I love being out in front and trying to find undiscovered gems, well before the crowd.

Having met with management and found Scott Wallace to be a smart and capable CEO, I’m very excited about the product expansion and product diversification strategy. It is set to ramp up in late Q4 FY 2024 and early 2025, with the upcoming production of the Toyota FJ Cruiser and 1967 and 1968 Ford Mustang lines.

In addition, the company benefits from a tiny public float, so if the investing public were to stumble upon/ discover this story, the short sellers might have a tough time actually locating and delivering shares to cover.

In closing, this ticks all the boxes when I’m questing for a unique and compelling micro-cap stock.

Appendix

Pictures from the 3rd annual Nantucket Defender Rally:

Exhibit A:

Author’s photo

Exhibit B: An ECD model.

Author’s photo

Exhibit C: An ECDA custom build, as a customer happened to be visiting Nantucket, while the Defender rally was taking place. I met a nice couple from Colorado who owns this model.

Author’s photo

Exhibit D: I believe over 50 custom Defenders attended the rally.

Author’s photo

Editor’s Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.

link